(BSE: 513269 | NSE: MANINDS | ISIN: INE993A01018)

Company Background Man Industries (India) Ltd, the flagship company of the Man Group, UK, manufactures steel line pipes for high and medium pressure applications such as oil and gas, petrochemical and water transportation, anti-corrosion coating systems and aluminum extrusion products. The company started operations in 1989 as an aluminium extrusion company with an installed capacity of 4,000 tonne per annum (tpa). In 1994, it set up a Submerged Arc Welded (SAW) pipe plant in Pithampur, Madhya Pradesh. In 1998, it became an integrated SAW pipe manufacturer with its own polyethylene-coating facility as part of its forward integration plan. It also set up a spiral pipe-making mill. In FY05, the company expanded capacity by setting up another plant in Anjar, Gujarat. Post expansion, the combined capacity increased to 2,000 km of pipes per annum.

Investment Rationale Robust global demand boom Demand for SAW pipes is likely to remain firm in next five years due to burgeoning crude prices and depleting oil reserves. We expect global demand to be in the range of 67 million tonnes with around 66% flowing in from Middle East, Asia & US, the key markets for the Indian players. While demand in Europe and Russia would be met by internal supplies, demand in Middle East and US is likely to be met through imports. This high demand, coupled with supply constraints, would keep prices firm at for least two years through CY08 and 09, escalating to mid 2010, where after it may start softening.

Diversification the key attraction Man Industries’ business would be split equally between LSAW and HSAW pipes from December 2007. HSAW pipes are manufactured from hot-rolled (HR) coils, which is easily available at comparatively lower price. In contrast, LSAW are manufactured from plates, which are in short supply. Though the two types of pipes are interchangeable, the high price of LSAW pipes may put pressure on demand. The diversification would de-risk its business. Despite their high price, we believe LSAW pipes would continue to score better than the HSAW in terms of profitability as manufacturing cost of LSAW is around 50% that of HSAW. Further, the scrap generated from LSAW is also minimal. The yield in HSAW is 90-96% while that in LSAW is as high as 99.5 100%. Currently, the difference in prices for plates (raw material for LSAW) and hot rolled coils (raw material for HSAW) is between US$250-300 per tonne for different grades of steel. A lot of units to manufacture plates are being set up and we expect prices to decline in the next few years. We expect prices of plates to fall and the price differential between plates and coils will decline to US$0-100. We believe lower raw material prices would result in LSAW prices decline.

Timely capex, robust order book gives earning visibility Man Industries is in capex mode and post expansion, its capacity of 1 million tonnes would be more than 2x the existing capacity, equally distributed between LSAW and HSAW pipes. This would reduce the risk and increase the size of addressable market. With a robust order book position of Rs 2,400 crore, we expect the top line to grow at a CAGR of 51% over FY07-09E and net profit by 67%. Capacity utilization should be at about at 40% in FY09E.

Risk and Concerns Man Industries exports its products mainly to companies in the Middle East. About 90% of the current orders are from abroad. Any appreciation in the rupee could impact the company’s financial performance. Freight cost is an important cost for pipe manufacturers. A rise in freight charges could the bottom line. Capacity expansion by other players around the world or by new entrant may put pressure on realizations. A large number of players could result in the bargaining power of buyers increasing and manufacturers would not be able to pass on rises in raw material costs to buyer.

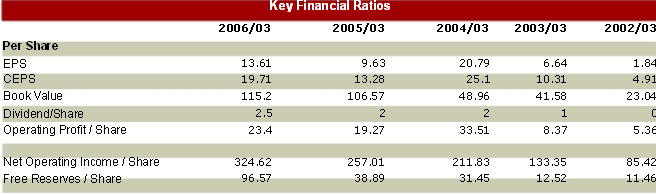

Financials In FY07, the company reported a top line of Rs 1,133.10 crore and a bottom line of Rs 55.30. In the Q108, sales grew 54% y-o-y to Rs 320.99 crore while bottom line grew 67% y-o-y to Rs 17.35 crore. The plant at Anjar started operations whereby the company increased the execution of new orders. Moreover, the company also witnessed traction in capacity utilization to around 45% on the current capacity of 600,000 tpa. From Q408, we expect the company would operate at the total capacity of 1 million tonnes. We expect the robust order book to drive the company’s top line at a CAGR of over 51% during FY07-09E to Rs 2,116.25 crore and bottom line at a CAGR of around 67% to Rs 153.71 crore.

Valuations Man Industries is set to capitalize on the rising global demand for pipelines. At the current price of Rs 255, the stock is trading at 4.42x the FY09E EPS. We expect orders from oil & gas clients to drive the growth momentum going forward and expect the stock to touch Rs 306, an upside of 20%, within a 3-6 month timeframe.

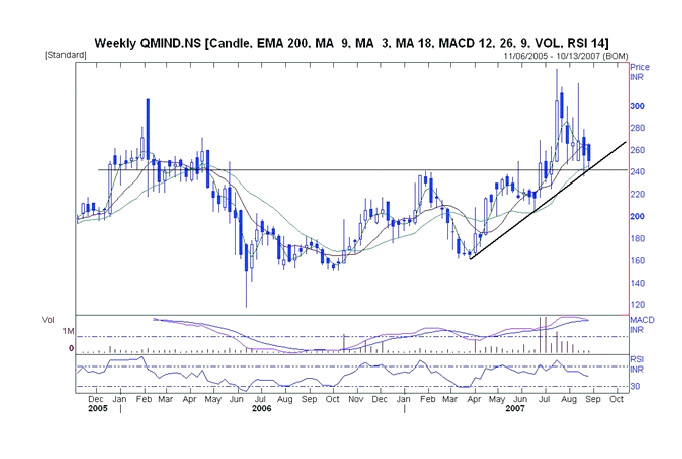

Technical Outlook The stock has broken above a long-term resistance at Rs 240. It had thereafter hit a high of Rs 320. It has now begun consolidating and is finding support at Rs 240. It has also formed a bullish rounding bottom formation. Momentum indicators remain in overbought zones. They are expected to come down after the consolidation before the next bullish impulse begins.

Other Info: Corporate Announcements | Board Meetings | Financial Results | Corporate Actions

Company Address | Shareholding Pattern | Results Comparison

Every week, the ICICIdirect research team selects a stock based on fundamental and/or technical parameters, which is likely to give a return of 20% or more over a 3-6 month perspective.

Investment in equity shares has its own risks. Sincere efforts have been made to present the right investment perspective.The information contained herein is based on analysis and up on sources that we consider reliable. I, however, do not vouch for the accuracy or the completeness thereof. This material is for personal information and I am not responsible for any loss incurred based upon it.& take no responsibility whatsoever for any financial profits or loss which may arise from the recommendations given in this blog.