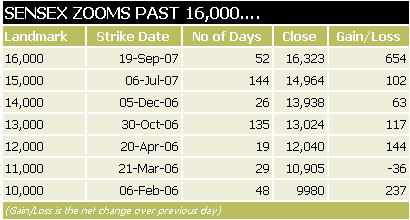

The Sensex opened with a bang at a new all-time high of 15,941 - up 272 points from its previous close - on the back of positive global cues. The US Fed, on Tuesday, cut its benchmark rate by 50 basis points, for the first time in four years, to 4.75%. A move that resulted in a strong rally across the globe. The buying momentum was so strong that the Sensex soon crossed a new landmark of 16,000, and went on to extend gains as the day progressed. The index hit an all-time, intra-day high at 16,335 - up 666 points from the previous close. The Sensex finally ended with its biggest-ever single-day gain of 654 points at 16,323.

The index took only 52 trading sessions to move from 15,000 to 16,000. While the BSE Mid-cap index advanced nearly 2% to 7117, the Small-cap index added 1% to 8871. The BSE Realty index surged 5.8% to 8465. The Bankex and Oil & Gas indices rallied nearly 5% each to 8691 and 8924, respectively. The market breadth was positive - out of 2,850 stocks traded, 1,541 advanced, 1,233 declined and 76 were unchanged.

BIG MOVERS… All the Sensex stocks ended with gains today. HDFC and HDFC Bank zoomed nearly 8% each to Rs 2,354 and Rs 1,326, respectively. Bharti Airtel soared 6.5% to Rs 886. ONGC surged 6% to Rs 902, and Maruti was up 5.8% at Rs 926. Reliance rallied 5.5% to Rs 2,173. Reliance Communications and ICICI Bank gained 5% each at Rs 564 and Rs 970, respectively. Tata Steel and Bajaj Auto moved up 4.7% each to Rs 745 and Rs 2,512, respectively. While Mahindra & Mahindra and SBI advanced 4.5% each to Rs 741 and Rs 1,770, respectively, Tata Motors and ITC added 3.7% each to Rs 722 and Rs 187, respectively. Hindalco and Infosys were up 3% each at Rs 159 and Rs 1,853, respectively. ACC surged 2.7% to Rs 1,153.

MOST ACTIVE COUNTERS DLF topped the value chart with a turnover of Rs 255.70 crore followed by Reliance (Rs 227 crore), ICICI Bank (Rs 148.70 crore), Reliance Capital (Rs 137.65 crore) and Renuka Sugar (Rs 127.80 crore). IKF Technologies led the volume chart with trades of around 1.85 crore followed by Ispat Industries (1.82 crore), Balrampur Chini (1.08 crore), IFCI (89.70 lakh) and Himachal Futuristic (87 lakh).

Sensex at16000: Experts say more gains to follow The Sensex closed above 16,000-mark for the first time, and market experts feel more gains will follow with some hiccups on the way.Though nobody is taking a call on where the index will be in the near-term, experts, across-the-board, continue to be bullish on Indian equities.

Nimesh Kampani, chairman, JM Financial : The basic issue is that the way the markets have gone up. The flow of FII money will increase in India and that is the expectation of the market. With the interest rates being cut, the appreciation of rupee, and looking at the rise in Asian markets today, it can be assumed that there has been a flow of FII money into the Asian markets. Sectors such as infrastructure, cement, steel and power look good, as we expect growth in these sectors.

Rakesh Jhunjhunwala, billionaire investor and stock trader : I’m and I have been bullish on the Indian markets. There is no change in my view

S Ramesh, COO, Kotak Investment Banking : Markets will be driven by liquidity, and money will move into markets like India where the growth story remains intact. The rise from this level will be driven by sectors like banking, construction and engineering. We are just coming out of a global meltdown, and the rise from here will be sector-specific and global-event driven.

Krishnamurthy Vijayan, CEO, JP Morgan Asset Management : We believe that since India is one of the best investment opportunities in the next few years, we will continue to attract investments - onshore and offshore. We have been consistently overweight on sectors that capture the Indian growth story, and have been underweight on auto and downstream oil.

Vijai Mantri, CEO, Deutsche AMC : We are very positive on India. The Indian growth story is completely driven by domestic demand. While there may be some bouts of volatility, I don’t see any constraint on corporate earnings growth. We are very bullish on capital goods, engineering and power. I think Indian markets are fairly valued but India may see a rate cut taking cues from FOMC.

Alok Vajpayee, CEO, Dawnay Day AV : The Indian market is following the global trend. I will not be surprised to see it at a much higher level. Some ups and downs will be there, but we will continue to see markets moving up. There could be a rate cut in India. There is lot of momentum in liquidity in Indian markets and I think they are at a fair valuation. Investors should look at specific companies rather than across-the-board buying. Second quarter results will be in line with our expectations.

Ramesh Damani, member, BSE : Markets have clinched 16,000 with a huge bang. Bulls are going to be in command. It reflects the strength of the Indian economy. We can say that it is India’s time under the sun. The road from here onwards looks very good. India’s domestic story is being driven by corporate fundamentals and earnings that are very strong. I am bullish on domestic sectors like logistics, cement, banking and underweight for the time being on technology. May be by Diwali this year, we can expect a rate cut.

Amar Ambani, Vice President (research), India Infoline : The 50bps rate cut by the Fed, the first in over four years, has keyed up global markets as well as Indian equities with investors breathing a sigh of relief. Talking about Indian markets in particular, the Fed cut, along with control over inflation and an improved political situation, has helped boost enthusiasm. A look at the advance tax figures also suggest that quarterly numbers are likely to be healthy. The feel-good factor of the Fed verdict will continue for some more time with increasing inflows in India where there are some very good investment opportunities.

Suyash Choudhary, Fund Manager, StanChart Asset Management : By delivering a 50 bps cut in the federal funds rate yesterday, the Fed has aimed at countering the detrimental effect on the broader economy arising from the tight credit conditions. The move has been accompanied by a cut by 50 bps on the discount window, which will further facilitate liquidity transmission into the financial system. While bonds world-wide are still cautious, equities have reacted very positively to the Fed move. Given that the move will help in restoring global financial stability, it is likely to positively affect domestic asset markets as well.

Ritesh Jain, Fund Manager (Debt), Principal Mutual Fund : The change in the Fed policy reinforces our near-term view on the benign interest rate environment. Inflation risk should continue to subside in this environment and will lend an element of flexibility to policy. The foreign flows in emerging markets may look up putting pressure on the domestic currencies to appreciate. The central bank may have to intervene aggressively to stem the uptrend in local currencies adding to domestic liquidity. While equity flows into emerging markets are likely to be good, the markets will also be watching for the corporate earnings in the current quarter. We expect the markets to remain strong. With the global interest rate environment turning benign and with most of the prominent central banks changing their stance in favor of growth than their concern on inflation, we may see even the domestic yield curve shifting lower over a period of time.

Kaushal Sampat, Chief Operating Officer, Dun & Bradstreet India : The cut in the Fed rate is likely to have some impact on the Indian economy. The widened interest rate differential between India and the US could result in a further surge of capital inflows (especially FIIs), which may lead to an appreciation of the rupee. The RBI may be under pressure to intervene in the forex market to preclude appreciation of the rupee beyond its comfort zone. The RBI could consider a decline in interest rates given the recent dip in the growth rate of industrial production and inflation being at a 17-month low thereby allowing the excess liquidity to flow into the economy through increased credit off take.

Sandeep Nanda, executive vice president (research), Sharekhan : The 50bps rate cut by the US Fed was ahead of expectation and thus a positive surprise. This prompt action has allayed concerns about a slowdown and will be positive for equities across the world including India. We expect cyclical and interest rate sensitive sectors such as banks, autos, metals to do well. There will now be greater pressure on the RBI to cut interest rates in India, which should boost earnings growth in FY2009.

Kunj Bansal, CIO (portfolio management services), Religare : With the FOMC announcing a 0.5% cut in the rate, the debate of an impending slowdown in the US has only increased. Moreover, the exact magnitude of the subprime crisis is yet to play out. Signals from Europe and Japan are not as salutary as they were in July. Crude has resumed its relentless pursuit of a three-figure price after a brief pause. These developments portend a steady increase of lows to those economies, which are essentially growing due to the domestic demand factor.

Therefore, India would stand to benefit as a consequence. That does not mean that everything is fine in the domestic space and that we are likely to see an out performance across sectors. The political undercurrents are far from positive. Further, the latest set of IIP numbers has revived the talk of a possible slowdown in the industrial growth going forward. The performance of the monsoon, on the other hand, has given sufficient reason for cheer. In essence, what we are saying is that whereas directionally there is nothing much to worry as far as the way forward is concerned, and the markets shall continue their northward journey. However, intermittent blips cannot be ruled out.